Featured resources

CPA Exam Review course free trial

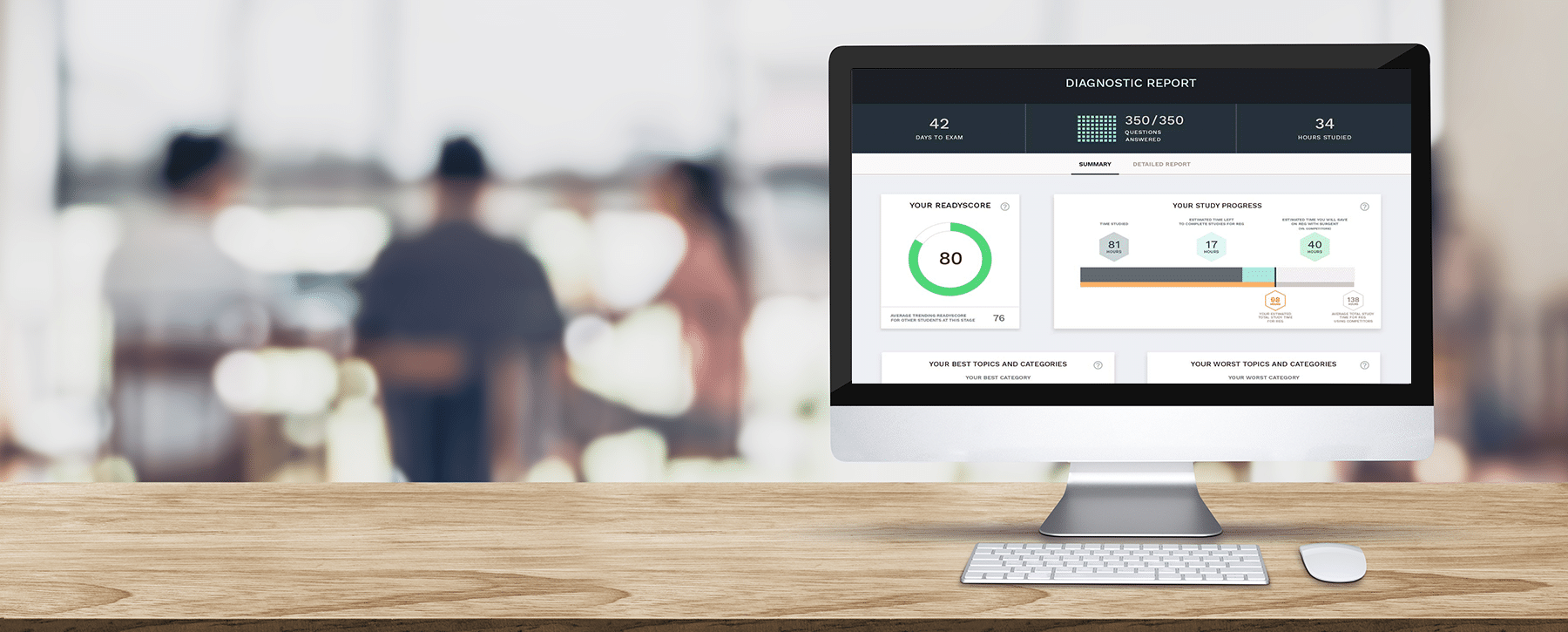

Try it out and see how our students study less and pass sooner.

More resources

Stay in the loop

Sign up today for can’t-miss industry updates, exam changes, and exclusive study tips from our expert blog.

- 5 Pioneering Black Figures in the Finance and Accounting Industries

February is Black History Month, a time to bring awareness to the many contributions Black Americans have made throughout our history despite institution and overt racism among other barriers. Here are five Black figures from history who paved the way for other Black Americans to… Read more: 5 Pioneering Black Figures in the Finance and Accounting Industries

February is Black History Month, a time to bring awareness to the many contributions Black Americans have made throughout our history despite institution and overt racism among other barriers. Here are five Black figures from history who paved the way for other Black Americans to… Read more: 5 Pioneering Black Figures in the Finance and Accounting Industries - Failed the EA Exam? 5 Things You Should Do to Ensure You Pass

Failing the EA Exam can be disheartening, but it’s not the end of the world. In fact, it’s an opportunity to reassess your study approach and come back stronger. Whether you’re retaking the exam or starting fresh, adopting effective study strategies is key to passing.… Read more: Failed the EA Exam? 5 Things You Should Do to Ensure You Pass

Failing the EA Exam can be disheartening, but it’s not the end of the world. In fact, it’s an opportunity to reassess your study approach and come back stronger. Whether you’re retaking the exam or starting fresh, adopting effective study strategies is key to passing.… Read more: Failed the EA Exam? 5 Things You Should Do to Ensure You Pass - 5 Reasons to Take Tax Prep Courses With SurgentLarge chains have long dominated the landscape in the tax preparation world. However, with their prominence come many drawbacks that can limit your potential as a tax professional. With their sprawling networks and ubiquitous storefronts, these industry titans have undeniably shaped the landscape of tax… Read more: 5 Reasons to Take Tax Prep Courses With Surgent

- Time Management Study Tips for the CMA ExamProfessionals who have earned the prestigious CMA certification understand the value of continued education and the commitment it requires. However, with demanding schedules and responsibilities, finding time to study and prepare for CMA exams can be a significant challenge. In this fast-paced environment, it’s essential… Read more: Time Management Study Tips for the CMA Exam

- 5 Benefits of Taking Tax Prep Courses With SurgentAre you considering a career change or seeking a flexible opportunity to boost your income? Look no further than tax preparation. In today’s dynamic economy, tax preparers are in high demand, offering a pathway to financial independence and career fulfillment. At Surgent Income Tax School,… Read more: 5 Benefits of Taking Tax Prep Courses With Surgent